Do you wonder if buying a property now is a good time or should you hold off a little longer in the hope that the stars will align more perfectly for you?

Can you as a buyer afford to be more patient and wait for your dream property to become cheaper?

Reserve Bank lifts official cash rate

Rate rises by the Reserve Bank of Australia (RBA) are now coming in quickly with the cash rate having risen from 0.1 per cent in April to 1.85 per cent this month. Interest rates are now the highest they have been since 2016. And while these increases are not unexpected, there is no doubt many of us are wondering for how long these rate increases will continue and what impact will it have on the property market.

There is a touch of optimism in the RBA Governor’s statement regarding future interest rate increases when he says:

‘The Board expects to take further steps in the process of normalising monetary conditions over the months ahead, but it is not on a pre-set path. The size and of future interest rate increases will be guided by the incoming data and the Board’s assessment of the outlook for inflation and the labour market’.

Our Federal Treasury’s latest forecasts show inflation to peak at 7.75 per cent by the end of the year, but it will take some time for it to come back down again.

When will interest rates stabilise?

The difficulties in predicting when inflation and interest rates will start to stabilise became most recently apparent when two major global organisations came out with very different forecasts for 2023. In their most recent “Global Economics Prospects” report, the World Bank lowered their forecasts for growth and warned that the world was in for several years of below average growth and above average inflation. In contrast, the OECD was more positive and forecast that inflation should start to ease by the end of the year.

For now, we are looking at continued increases in interest rates until the end of the year while inflation peaks at the same time.

House prices may be dropping, but can buyers celebrate yet?

Rising interest rates are the main factor being credited for the property market’s recent downturn. While in previous years, waiting to purchase may have meant being priced out of the property market as house prices continued to boom, the recent slowdown has buyers optimistic about what they might be able to achieve by holding fire. However, property prices may be dropping but that doesn’t mean that buyers are suddenly celebrating.

Lenders are simultaneously winding back how much people can borrow for mortgages as they factor in higher interest rate repayments and cost of living pressures.

Maximum home loan sizes are shrinking

Clearly, higher interest rates are eroding buyers’ borrowing power. A young couple were just told by their mortgage broker that their borrowing capacity has dropped by more than 10 per cent. That’s compared with a national property price drop of just 2 per cent since the beginning of May, according to property analytics firm CoreLogic. Whilst you wait, your dream home may be coming down in value, however your borrowing capacity may be decreasing much more…

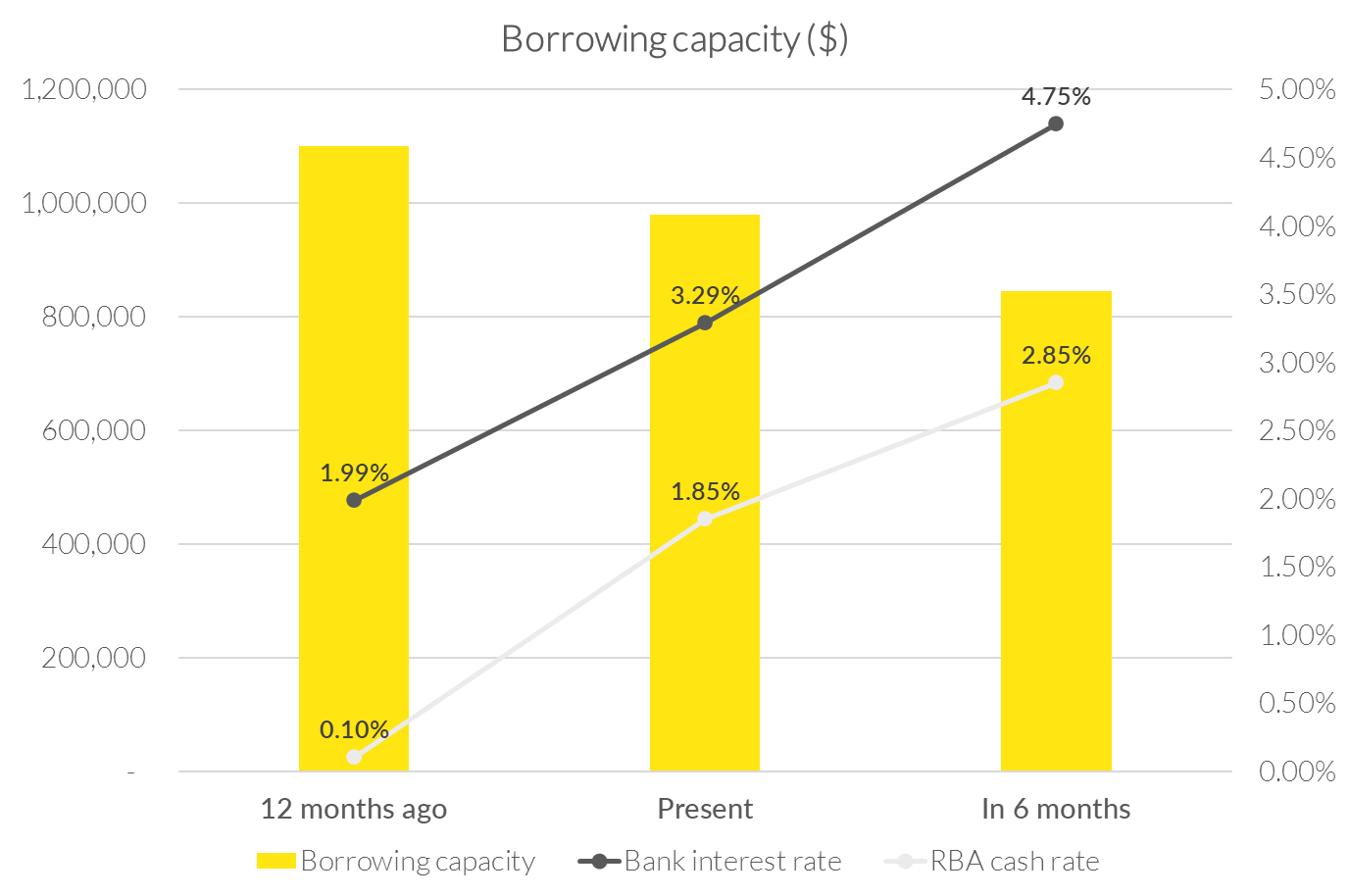

The couple were first approved for a mortgage of around $1,1 million 12 months ago, and then again when they went back for pre-approval earlier this year. That’s when Australia’s official cash rate was still at 0.1 per cent and their bank interest rate at 1.99 per cent.

Despite the new lending environment, the couple wasn’t expecting their estimated borrowing capacity to drop down from $1,1 million to $980,000 when they went back to their broker today and their new bank interest rate is 3.29 per cent.

Should the couple hold off for maybe a bit longer and wait for the interest rates to stabilise at the end of the year? We strongly believe with the interest rates continuing to rise, now is the best time to secure your dream home. In 6 months, the borrowing capacity for this couple will decrease from $980,000 to $845,000 if the RBA cash rate increases to 2.85 percent and their bank interest rate increases to 4.75 per cent.

See graph below how this couple’s borrowing capacity has been impacted by the interest rates:

If you are looking to buy a property or are thinking of buying a property, simply submit your contact details below and one of our agents will reach out to you.